Interactive Deck

Please enter the password you were sent.

Please enter the password you were sent.

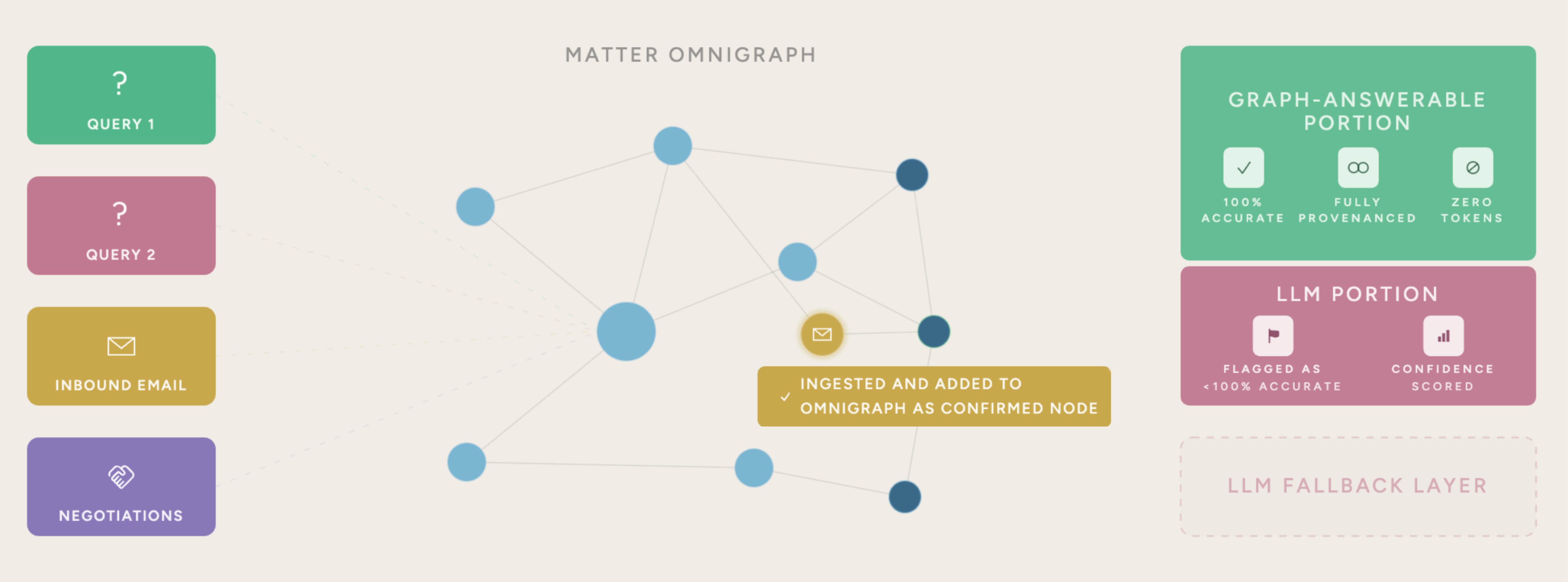

Our product platform, Matrix, structures and expresses every moving part in any given matter — whether a term, clause or email — in a live-updated, single-source-of-truth graph that all human and agentic queries are first routed to. The Omnigraph is centralised and authoritative as it pulls live data from across tools such as DMS (e.g. iManage), emails, DocuSign, etc.

The Omnigraph deterministically resolves ~85% of queries with provenance (hence the zero-hallucination guarantee assuming accurate ETL pipelines enforced by the human-in-the-loop); only queries it cannot answer are ever re-routed to the probabilistic LLM layer, flagged as such and confidence-scored. This graph-first infrastructure makes LLM outputs trustworthy.

Scan to see the Omnigraph animation in your browser — best on desktop.

Harvey ~$11B. Legora $100M+ ARR. Centari $14M. Ontra $310M+. Willingness to pay is settled; architecture isn't.

Every funded player is LLM- or document-first. None graph-native. Harvey's $200M Series D went to agents, not foundations.

Harvey shipped agents March 2026. Deploying agents without a deterministic trust layer is liability waiting to happen.

EU AI Act high-risk obligations live 2 Aug 2026. SRA demands explainability across 200,000 E&W solicitors.

Every matter produces an Omnigraph — a training signal for the next matter, firm, practice area. Data accumulates inside the architecture, not on top of it.

Every fund structure, deal type, side letter extends the ontology. A 2027 entrant will need years of edge cases to catch up.

1,000 matters = 1,000 living omnigraphs feeding the precedent library. Migrating off means walking away from years of institutional knowledge.

Every cross-firm transaction is a Matrix-to-Matrix handshake. The network spreads sideways through deals, not top-down through sales.

anyone with a whiteboard and sufficient domain knowledge can sketch the graph schema specific to each practice area. It's the structured data crystallising inside that architecture, matter by matter — institutional memory competitors would need years of edge cases to replicate. Whoever ships graph-native first, owns the compounding.

Two BAME, female, socially mobile lawyers. One bedroom startup founded 7 years ago that became the multi-award-winning social mobility charity, STRIVE Talent. Now building the intelligence layer that transactional lawyers have needed for decades. Between them: the transactional legal experience and the technical vision to build what nobody else has thought to build in quite this way.

Six years at top fund practices in the City; formation of funds with AUM in the billions is her bread and butter. She has done, manually, everything Matrix is built to replace. Sana does not have a theory about how transactional lawyers work: she is one. She has sat in every closing, negotiated every side letter, and managed every MFN process that Matrix handles. When she says the current workflow is broken, she means she lived it — just last Thursday. She is the domain expert on call who shapes design and schema decisions, tightening the feedback loop from months to minutes.

Chancery-trained barrister. Silver-circle trained solicitor. 42-trained software engineer with systems/architecture depth and product/design instinct. She has acted for Deutsche Bank, Goldman Sachs and Barclays on transactions up to £350M, then as Chief of Staff at a fast-scaling professional services firm drove 40% revenue growth while digitising its entire client base. Her capability as a high-resolution translator between Sana's domain expertise and her varied skills stack means we can execute at breakneck velocity, with crystal clarity of vision, and stay leaner for longer.

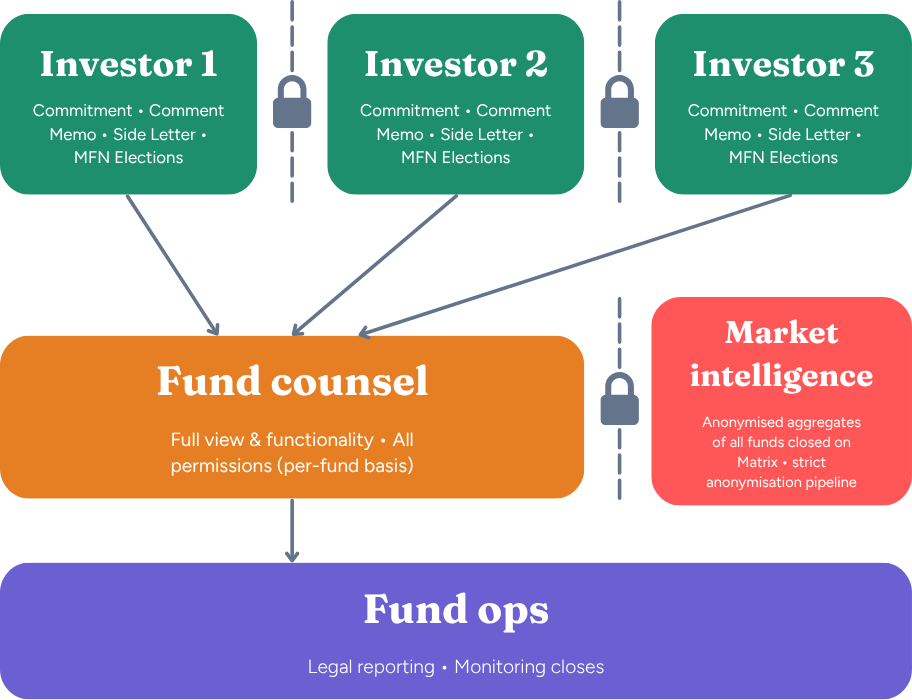

Isolation enforced at the architecture layer — not just the UI — with role-based access and EU / UK / US data residency. Here is an example diagram of how InfoSec would look for fund formation, but the same principles apply across Finance and M&A.

Each investor's side-letter terms, negotiation history and concessions are stored in discrete, permissioned nodes. No investor can query, view, or infer another's position. Confidentiality is enforced at the architecture layer, not just the UI.

Every user operates within a defined permission tier — Fund Counsel (full fund view), Fund Ops (operational data only), Investor Counterparty (own data only). Queries requiring graph traversals beyond each user's permissions will be denied. Access is logged, timestamped and auditable.

Matrix's cloud infrastructure is deployable with EU-based data centres (AWS Frankfurt / Dublin or Azure Netherlands / Ireland) for GDPR-bound funds, UK regions for post-Brexit clients, and US-East / US-West for US clients. Region selection is configured at onboarding and documented in the Data Processing Agreement.